Managing your money is very important but some people often ignore its importance. A budget is like a guide which helps you to manage your money and achieve your future goals. So, this blog will show you why budgeting matters so much. It will also explain different ways to budget and its best tools.

The Importance of Budgeting

A budget is more than just a spreadsheet or a collection of numbers; it’s a strategic plan for your money. It provides a clear picture of your income and expenses, allowing you to make informed decisions about how you earn, spend, save, and invest. Here’s why budgeting is important:

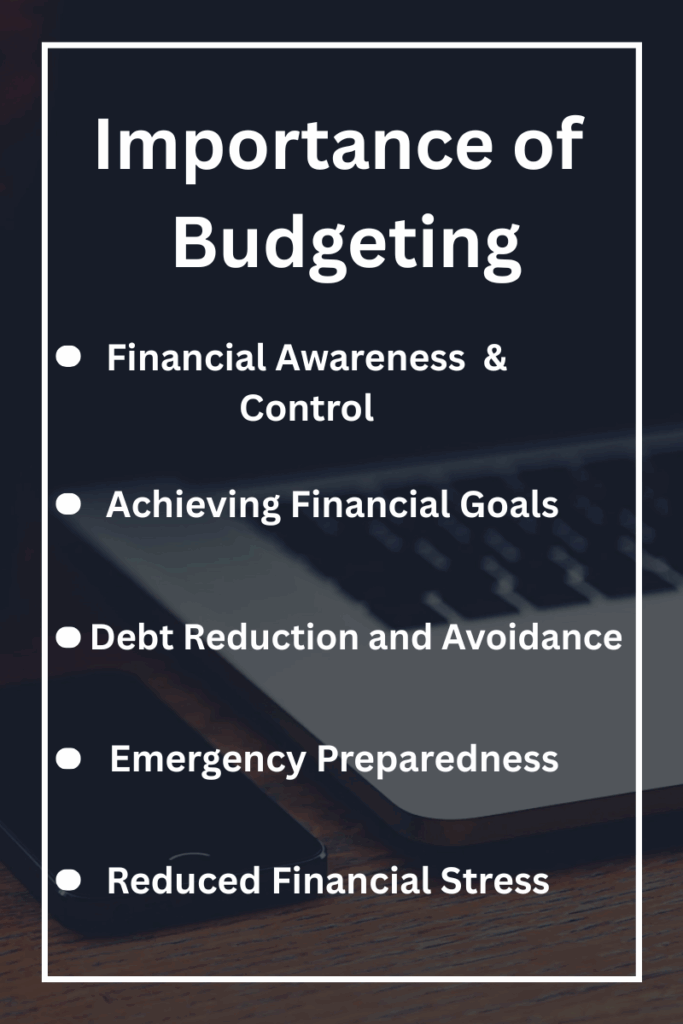

- Financial Awareness and Control: Many people operate without a clear understanding of where their money goes. Budgeting illuminates your spending habits, revealing areas where you might be overspending or underspending. This awareness is the first step toward gaining control over your finances.

- Achieving Financial Goals: Whether your goal is to save for a down payment, pay off debt, or retire early, a budget provides the roadmap. It helps you allocate funds strategically to reach your objectives within a defined timeline.

- Debt Reduction and Avoidance: Debt can be a significant burden. A budget helps you identify how much extra money you can allocate towards debt repayment, accelerating your path to becoming debt-free. It also prevents new debt by ensuring you don’t spend beyond your means.

- Emergency Preparedness: Life is unpredictable. Unexpected expenses like medical emergencies, car repairs, or job loss can derail your financial stability. A budget helps you build an emergency fund, providing a safety net during challenging times.

- Reduced Financial Stress: Financial worries are a leading cause of stress. When you have a clear understanding of your financial situation and a plan in place, you experience greater peace of mind and reduced anxiety.

Budgeting Methods: Finding Your Fit

There’s no one-size-fits-all approach to budgeting. The best method depends on your financial situation, personality, and comfort level with tracking. Here are some popular budgeting methods:

The 50/30/20 Rule

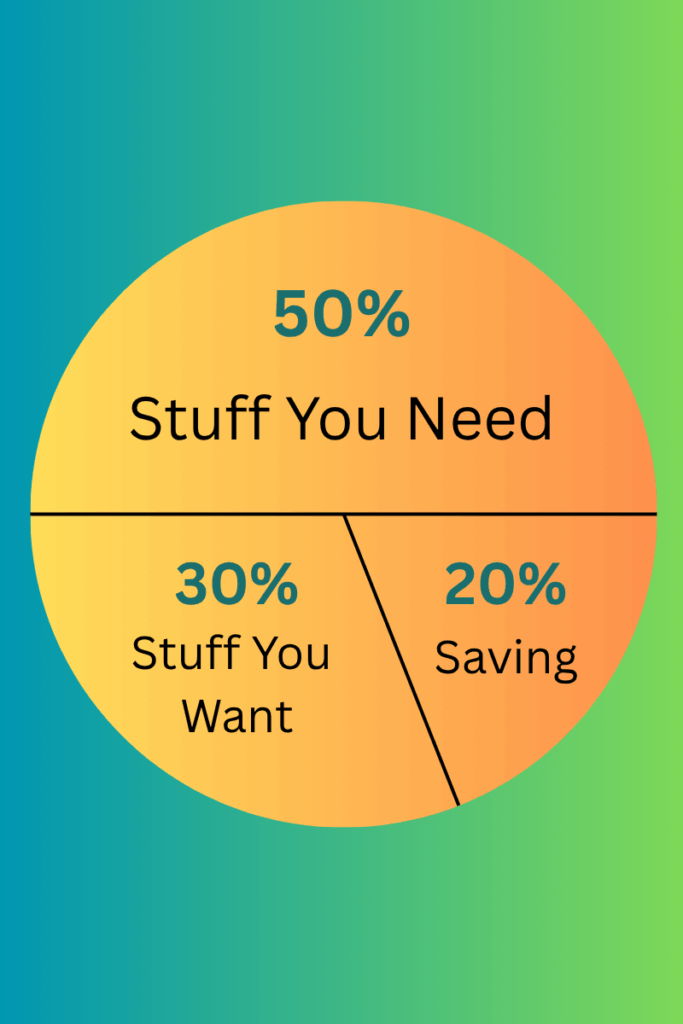

“The 50/30/20 Rule” is a super easy way to manage your money. Imagine your take-home pay (the money you get after taxes) as a pie. This rule tells you how to slice up that pie.

- 50% for Stuff You Need: This is the biggest slice, and it’s for all the absolute essentials you can’t live without. Think of things like rent or house payment, electricity, water, heater bills, groceries, health or car insurance.

- 30% for Stuff You Want: This is the next slice, and it’s for all the things that make life fun and enjoyable but aren’t strictly necessary. For example- eating out at restaurants, going to the movies or concerts, subscriptions like Netflix or gym memberships, hobbies, vacations.

- 20% for Saving & Paying Off Debts: This is the final, very important slice. This money is dedicated to making your financial future better. It goes towards saving (building up an emergency fund, saving for a down payment on house).

Zero-Based Budgeting

Imagine you get paid, and you have a certain amount of money in your hand. With Zero-Based Budgeting, you don’t just spend and hope for the best. Instead, you give every single rupee of that money a specific job before you spend it.

Think of it like this: You have ₹50,000 income. You decide ₹15,000 goes to rent. ₹5,000 goes to groceries. ₹2,000 goes to transportation. ₹3,000 goes to paying off a credit card. ₹10,000 goes into your savings account. ₹4,000 for entertainment. ₹1,000 for coffee and snacks.

You keep assigning a job to every rupee until you’ve assigned all ₹50,000. At the end, your income minus all your assigned expenses, savings, and debt payments should equal zero. It takes a bit more effort to track everything, but it gives you a very clear picture and a lot of power over your finances.

Thus, Total Income- Total Expenses=0

Envelope System

Imagine you get your paycheck, and instead of just putting all your money in one bank account, you divide it up right away for different things you need to buy. Here’s how it works:

- Get your money (cash): When you get paid, you take out the cash you plan to use for your expenses.

- Label your envelopes: You get a bunch of envelopes and label each one with a spending category. For example, groceries, eating out, clothes etc.

- Fill the envelopes: You decide how much money you want to spend on each category for the month (or week, whatever works for you) and put that exact amount of cash into the corresponding envelope. So, if you budget ₹10,000 for groceries, you put ₹10,000 cash in the “Groceries” envelope. ₹2,000 for eating out goes into the “Eating Out” envelope.

- Spend only from the envelopes: When you need to buy something, you take the money only from the correct envelope. For example, need money to buy groceries? Take money from the grocery’s envelope.

- When it’s empty, you’re done! This is the key part. If your “Eating Out” envelope runs out of cash, you simply cannot eat out again until you get your next paycheck and refill the envelopes. You stop spending in that category because there’s no more money physically available for it.

Think of each envelope as a mini budget for just one type of spending. Once that mini budget (the cash in the envelope) is gone, you know you’ve hit your limit for that item.

Paycheck to Paycheck Budgeting

Imagine you get paid, and instead of just wondering where your money will go, you immediately give every single rupee from that paycheck a specific job.

- “This much is for rent.”

- “This much is for groceries.”

- “This much is going into my savings.”

- “This much is for that electricity bill due next week.”

“Okay, I have ₹10,000 this payday. ₹3,000 for rent, ₹2,000 for food, ₹1,000 for transport, ₹2,000 for savings, and the last ₹2,000 for fun stuff.” And then you stick to that plan until your next payday. This is super helpful for people who don’t get a fixed salary every month (like freelancers or gig workers) because it helps them make sure they cover all their important bills and goals with the money they do have.

Tools to Support Your Budgeting Journey

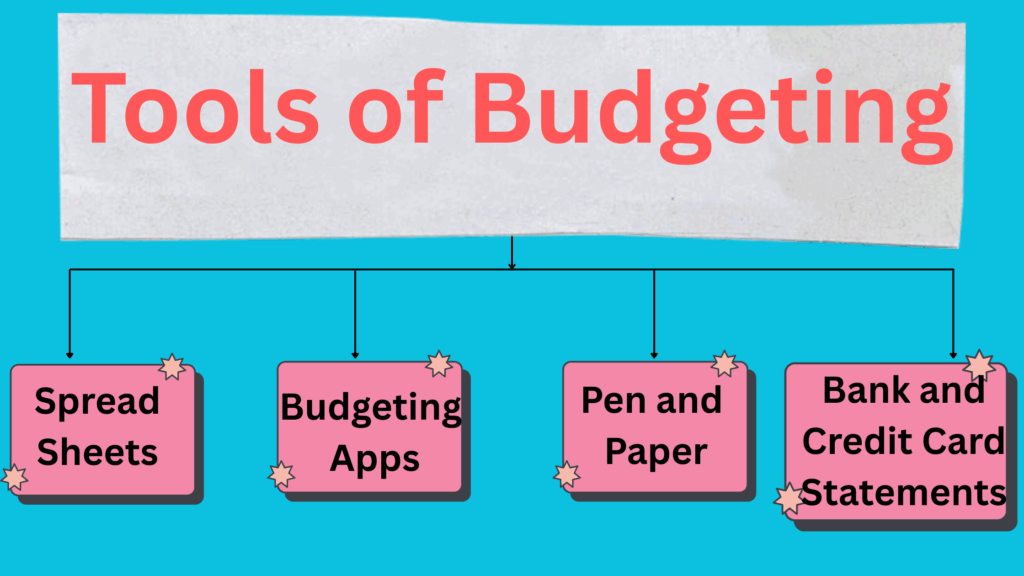

Technology has made budgeting more accessible. Here are some important tools of budgeting :

- Spreadsheets (Excel, Google Sheets): For those who prefer a hands-on approach and customization, spreadsheets are powerful tools. You can create your own budget templates, track income and expenses, and analyze your financial data.

- Budgeting Apps: Here are some important budgeting apps which are described as under:

- Mint: A free, popular app that links to your bank accounts, credit cards, and investments, automatically categorizing transactions and providing insights into your spending.

- YNAB (You Need a Budget): A paid app that emphasizes zero-based budgeting. It focuses on giving every dollar a job and planning for future expenses.

- Pocket Guard: Helps you track your spending, categorize transactions, and shows you how much “spendable” money you have left.

- Simplify by Quicken: Offers budgeting, spending tracking, and insights into your financial health, similar to Mint.

- Pen and Paper: For those who prefer simplicity and a tactile experience, a notebook and pen can be just as effective. This method encourages mindful spending as you manually record every transaction.

- Bank and Credit Card Statements: Regularly reviewing your bank and credit card statements is a fundamental part of budgeting, regardless of the method or tool you use. They provide a detailed record of your transactions.

Also Read: 24/7 Guide to Digital Savings Account

Creating Your Budget: A Step-by-Step Guide

Now that you understand the importance of budgeting and the various methods and tools, let’s walk through the steps to create your own budget:

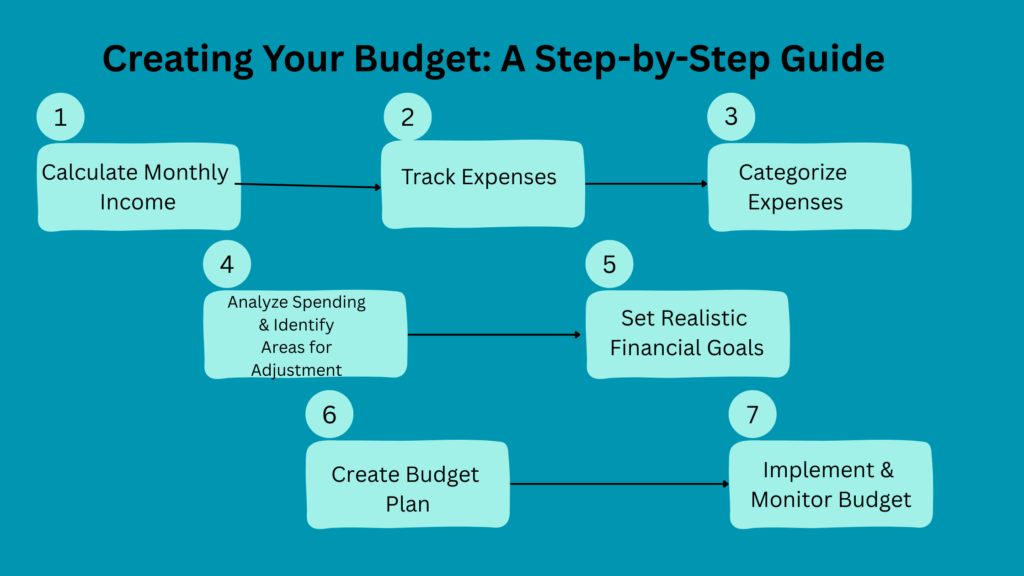

Step 1: Calculate Your Monthly Income: Start by tallying all your sources of income after taxes. This includes your salary, freelance income, rental income, benefits, etc. If your income varies, use an average of the past few months or a conservative estimate.

Step 2: Track Your Expenses: This is the most important step. For at least a month, track every single dollar you spend. This means logging your rent, groceries, transportation, dining out, subscriptions, and even that daily coffee. Categorize your expenses as fixed expenses and variable expenses.

Step 3: Categorize Your expenses: Group your tracked expenses into meaningful categories. Common categories include Housing, Transportation, Food, Debt Payments, Insurance, Personal Care, Entertainment, Savings.

Step 4: Analyze Your Spending and Identify Areas for Adjustment: Once you have a clear picture of your income and expenses, compare them.

- If Income > Expenses: Congratulations! You have a surplus. Decide how you want to allocate this extra money (e.g., increased savings, debt reduction, investments).

- If Expenses > Income: This means you’re spending more than you earn. Identify areas where you can cut back. Look at your variable expenses first, as they offer the most flexibility. Can you reduce dining out, cancel unused subscriptions, or find cheaper alternatives for certain services?

Step 5: Set Realistic Financial Goals: What do you want to achieve with your money? Set both short-term (e.g., build an emergency fund, pay off a small debt) and long-term goals (e.g., buy a house, retire early). Assign specific amounts and timelines to these goals.

Step 6: Create Your Budget Plan: Based on your income, expenses, and financial goals, create a detailed plan for how you’ll allocate your money for the upcoming month. Assign a specific amount to each expense category. Remember to be realistic and flexible.

Step 7: Implement and Monitor Your Budget: Start using your budget. Track your spending diligently to ensure you stay within your allocated amounts. This step requires discipline and consistency. Use your chosen tool (spreadsheet, app, or pen and paper) to record transactions regularly.

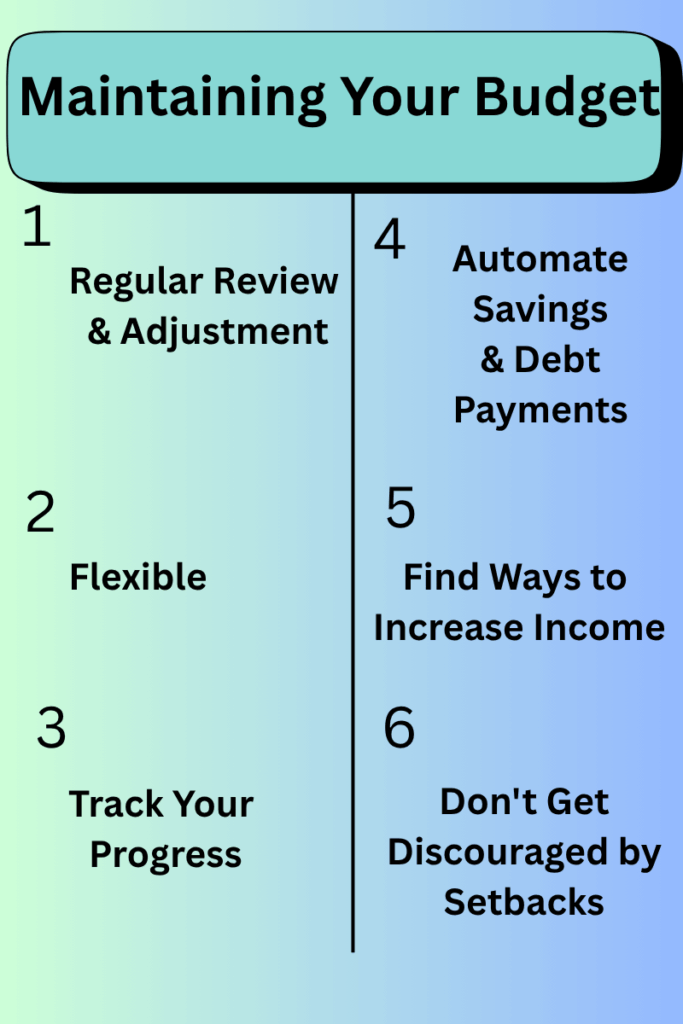

Maintaining Your Budget: It’s an Ongoing Process

Creating a budget is just the beginning. Maintaining it requires ongoing effort and adjustments.

- Regular Review & Adjustment: Review your budget at least once a month. Are your income or expenses different? Have your financial goals shifted? Make necessary adjustments to ensure your budget mains relevant.

- Flexible: A budget should not be rigid; it should always be flexible. There will be months where unexpected expenses happened. Don’t get discouraged if you go over budget in one category. Adjust and learn from it. The goal is progress, not perfection.

- Track Your Progress: Celebrate your successes! Seeing how much debt you’ve paid off or how much you’ve saved can be incredibly motivating.

- Automate Savings and Debt Payments: Set up automatic transfers from your checking account to your savings account or directly to your debt payments. This ensures you prioritize your financial goals and removes the temptation to spend that money.

- Find Ways to Increase Income (if necessary): If you consistently struggle to meet your financial goals with your current income, explore options to increase your earnings, such as a side hustle, negotiating a raise, or learning new skills.

- Don’t Get Discouraged by Setbacks: Everyone faces financial challenges. If you deviate from your budget, don’t give up. Simply acknowledge it, learn from it, and get back on track.

Budgeting Challenges to Overcome

Let’s break down those common budgeting mistakes in simple terms, like things you should really try not to do when you’re managing your money.

Being Unrealistic

- It’s great to want to save a lot, but if you suddenly try to cut out all your fun money or dramatically reduce your grocery budget when you know you spend a certain amount, you’ll probably get frustrated and give up.

- Example: You love coffee. If your budget says, “zero rupees for coffee,” you’ll probably buy coffee anyway, feel bad, and then think the whole budget is useless.

- Think of it like: Trying to run a marathon on your first day of exercise. You’ll just get tired and quit. Start with smaller, achievable goals.

Not Tracking All Expenses

- It’s easy to remember big bills like rent, but those small purchases – a ₹20 packet of chips, a ₹50 auto ride, a ₹100 online game – add up very quickly. If you don’t write them down, you’ll wonder where your money went.

- Example: You buy a few small things every day that you forget to note down. By the end of the month, those “small things” might be ₹1,000 or ₹2,000 that you didn’t plan for.

- Think of it like: Having a bucket with a bunch of tiny holes. If you don’t plug them all, the water (your money) will slowly leak out.

Getting Discouraged by Mistakes

- You’re going to overspend in a category sometimes. It happens! The important thing is to learn from it, adjust, and get back on track, not to get discourage.

- Example: You planned ₹500 for entertainment this week, but you spent ₹800 because a friend invited you to a concert. Don’t think “Oh well, my budget is ruined!” Instead, think “Okay, I spent extra. Next week, I’ll try to cut back a bit or make a note to plan for bigger events next time.”

- Think of it like: Learning to ride a bicycle. You’ll fall a few times, but you get back on and keep trying.

Ignoring Irregular Expenses

- Some expenses don’t come every month, but they’re still important – like your annual car insurance premium, house repairs, or paying for school fees once a year. If you don’t plan for them, they hit you hard when they arrive.

- Example: Your car insurance costs ₹12,000 once a year. If you don’t save ₹1,000 each month, you’ll have to find ₹12,000 all at once when the bill comes.

- Think of it like: Knowing a festival is coming up later in the year. You wouldn’t wait until the last minute to save for gifts, would you?

Not Envolving Everyone

- If you share money with a partner or family members, everyone needs to be involved in making the budget and understanding how it works. If only one person knows the plan, it’s very hard to stick to.

- Example: You budget for groceries, but your partner buys expensive takeout every day because they don’t know the food budget. This will cause problems.

- Think of it like: Trying to row a boat with only one person rowing and the other just sitting there. You won’t get far, or you’ll go in circles.

Conclusion

Budgeting is a powerful tool for taking control of your financial future. It provides clarity, reduces stress, and empowers you to make informed decisions that align with your financial goals. While it requires discipline and consistency, the rewards – financial freedom, peace of mind, and the ability to achieve your aspirations – are well worth the effort.

Lovart AI Agent is reshaping how we think about design automation, blending AI with creative control. The tri-modal interface is especially clever for intuitive workflows. Check it out at Lovart AI Agent.

Thanks for the visit