In our busy lives today, it’s all about making things easy and quick. That’s where the Digital Savings Account comes in. It’s totally a new and modern way to handle your money. It makes banking smooth, fast, and often give you better benefits than old-fashioned banks.

If you want to make your money management simpler, earn more interest on your savings, and be able to bank whenever you want (24/7), then a digital savings account is probably a great choice for you.

What is Digital Savings Account?

A digital savings account is basically a regular savings account, but everything is done online or through a mobile app. You don’t fill out any physical forms to open it. It’s all done digitally, like taking pictures of your ID with your phone. You don’t have to go to a bank branch for anything.

You can open the account, deposit money, withdraw money, and manage it all from your phone or computer. Just like your phone is always with you, your digital savings account is always accessible, 24/7. You can check your balance, make transfers, or pay bills whenever you want.

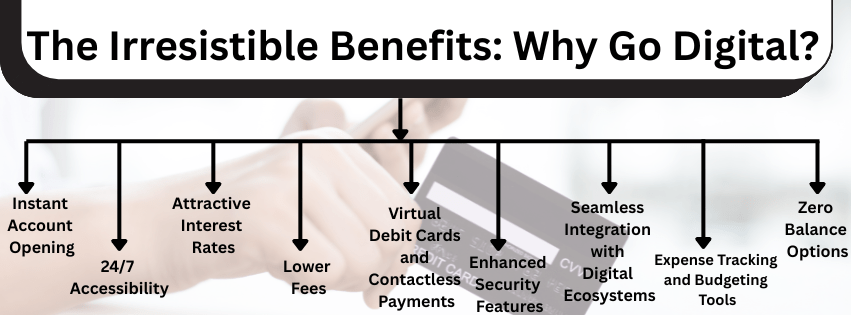

The Irresistible Benefits: Why Go Digital?

The shift to digital savings accounts isn’t just a trend; it’s a fundamental improvement in banking. Here’s a breakdown of the compelling advantages:

Instant Account Opening

Opening a bank account used to be a long and annoying process. You had to fill out lots of papers, hand in physical documents like your ID, and then wait for days before you could actually use your account. But with Digital Accounts, it becomes very fast and easy. You can do everything online, usually in just a few minutes.

They use a quick way to check your identity called Aadhaar-based OTP verification (which means they send a code to your phone linked to your Aadhaar ID) and video KYC (where you do a quick video call to show your face and ID). So, instead of all the paperwork, it’s completely paperless, which is not only convenient for you but also good for the environment.

24/7 Accessibility

Think of a digital savings account like having your bank in your pocket, always open. Instead of going to a physical bank branch to do things like get cash, see how much money you have, send money to someone else, pay your electricity bill, handle your investments.

You can do all of this directly from your phone or computer, at any time of day or night, even on holidays. You don’t need to worry about the bank being closed or if it’s too late to get there. It gives you complete control over your money whenever it’s convenient for you.

Attractive Interest Rates

Imagine traditional banks as having lots of physical shops (branches) with many employees. This costs them a lot of money to run. Digital banks, on the other hand, are like online-only stores. They don’t have those physical shops or as many employees, so their running costs are much lower.

In simple terms:

- Traditional Banks: High costs = Lower interest rates.

- Digital Banks: Lower costs = Higher interest rates.

Lower Fees

Digital savings accounts are a modern alternative to traditional bank accounts that can save you money. Unlike regular accounts, they usually have very low or no fees for things like monthly maintenance or taking cash out from ATMs. This means you get to keep more of your hard-earned money, making them a great choice if you want to grow your savings and avoid unnecessary costs.

Virtual Debit Cards and Contactless Payments

When you open a new digital bank account, you’re usually given an immediate virtual debit card. This card, which exists only online, lets you pay for things instantly on websites, online stores, and through various apps. On top of that, many accounts also provide a physical debit card.

This physical card often has “contactless” technology, meaning you can simply tap it at a store’s payment terminal to complete a purchase quickly and securely. Together, these cards make it easier and safer to pay for things without needing to carry cash.

Enhanced Security Features

Even though digital savings accounts exist online, banks take their security very seriously. They use strong measures to protect your money and information, such as requiring more than one way to verify your identity (like a one-time password or fingerprint), scrambling your data so others can’t read it, and constantly looking for any suspicious activity. Furthermore, the Reserve Bank of India (RBI) has strict rules in place that banks must follow to ensure all digital banking services are safe and secure for customers.

Seamless Integration with Digital Ecosystems

Digital savings accounts are designed to integrate seamlessly with various digital payment platforms (like UPI in India), investment apps, and online services. This creates a comprehensive financial ecosystem where you can manage your banking, investments, payments, and even loans from a single, integrated platform.

Expense Tracking and Budgeting Tools

Digital banking apps aren’t just for checking your balance; they often come with smart tools that act like your personal finance assistant. These tools automatically organize your spending, putting transactions into categories like “groceries,” “transport,” or “entertainment.”

This makes it easy to see where your money goes. Plus, you can set limits for how much you want to spend in each category, helping you stick to a budget. By having a clear picture of your spending, these features help you spot areas where you can save money and ultimately reach your financial goals faster.

Zero Balance Options

For many people with regular bank accounts, a big hassle is having to keep a certain amount of money in their account every single day, known as the minimum average balance (MAB). If they don’t, the bank charges them a fee.

But with many digital savings accounts, you don’t have to worry about this! They offer “zero balance” options, meaning you don’t need to keep any specific amount in the account, which is a huge relief and makes banking easier for more people to access.

Also Read: India’s Banking Sector Evolution: From 1947 Roots to Digital Revolution

Digital vs. Traditional: A Quick Comparison

While both help you save, digital and traditional savings accounts work very differently and offer distinct advantages.

| Feature | Digital Savings Account | Traditional Savings Account |

|---|---|---|

| Account Opening | Instant, paperless (video KYC, Aadhaar OTP) | Branch visit, physical forms, document submission |

| Accessibility | 24/7 via mobile app/web portal | Limited to branch hours, some online banking available |

| Fees | Often lower or zero fees (maintenance, ATM) | Can have various fees, minimum balance requirements |

| Interest Rates | Often higher | Typically lower |

| Physical Presence | Minimal or no physical branches | Extensive branch network |

| Card Type | Virtual debit card (instant), physical debit card also | Physical debit card |

| Features | Advanced budgeting, expense tracking, integrated services | Basic banking services, less integrated digital tools |

| Customer Service | Primarily digital (chat, email, in-app support) | Branch visits, phone banking |

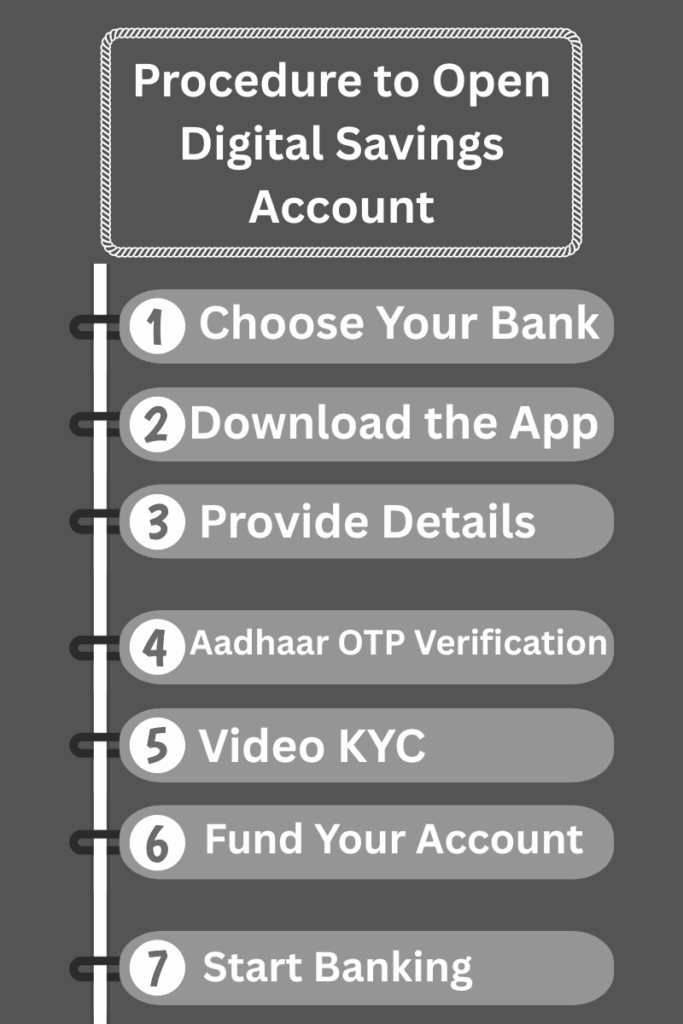

How to Open Your Digital Savings Account

Opening a digital savings account is typically a straightforward process:

- Choose Your Bank: Research different banks offering digital savings accounts. Compare interest rates, features, fees, and customer reviews. In India, many prominent banks like IDFC FIRST Bank, Axis Bank, Yes Bank, and payment banks like Fino offer compelling digital account options.

- Download the App/Visit Website: Download the bank’s official mobile banking app or visit their dedicated digital account opening page.

- Provide Details: Enter your personal information, including your name, mobile number, PAN card details, and Aadhaar card number.

- Aadhaar OTP Verification: Your mobile number linked with your Aadhaar will receive an OTP for verification.

- Video KYC: Most banks will require a quick video KYC call. This involves a bank representative verifying your identity by showing your original PAN card and Aadhaar card on camera.

- Fund Your Account: Once verified, you can instantly fund your account through various digital payment methods.

- Start Banking: Your digital savings account is now active! You can begin using your virtual debit card, setting up UPI, and exploring all the features of the mobile banking app.

Important Note on KYC: While digital accounts often allow for “minimal KYC” initially, the Reserve Bank of India (RBI) mandates completion of full KYC within a year of opening the account. Failing to do so might lead to restrictions or closure of the account. Full KYC typically involves a video call or a visit to a designated point.

Is a Digital Savings Account Safe?

Yes, digital savings accounts are generally very safe. Reputable banks offering these accounts adhere to strict security protocols and regulatory guidelines set by central banks like the RBI. Key security measures include:

- Encryption: All data transmitted between your device and the bank’s servers is encrypted.

- Multi-Factor Authentication (MFA): Requires multiple forms of verification (e.g., password + OTP or fingerprint) to access your account.

- Fraud Detection Systems: Banks employ sophisticated systems to monitor for suspicious activities and prevent unauthorized transactions.

- Virtual Card Security: Virtual cards often have features like single-use numbers or the ability to freeze/unfreeze them instantly.

- RBI Regulations: The RBI actively supervises and regulates digital banking operations, ensuring consumer protection and financial stability.

- Multi-Factor Authentication (MFA): Requires multiple forms of verification (e.g., password + OTP or fingerprint) to access your account.

- Fraud Detection Systems: Banks employ sophisticated systems to monitor for suspicious activities and prevent unauthorized transactions.

- Virtual Card Security: Virtual cards often have features like single-use numbers or the ability to freeze/unfreeze them instantly.

- RBI Regulations: The RBI actively supervises and regulates digital banking operations, ensuring consumer protection and financial stability.

However, as with any digital platform, it’s crucial for users to practice good digital hygiene. Always use strong, unique passwords, be wary of phishing attempts, and avoid sharing your credentials.

The Future is Digital: What to Expect

The landscape of digital banking in India is continuously evolving and expanding. We can expect to see:

Hyper-Personalization

Hyper-personalization in banking means that your bank will use smart computer programs (AI) and look at how you usually spend and save your money (data analytics). With this information, they can offer you special financial products, services, or advice that are perfectly suited just for you.

For example, if they notice you’re saving for a house, they might suggest a specific home loan with better terms, or if you frequently travel, they might offer a credit card with great travel rewards. It’s like having a personal financial assistant who knows your habits and goals, giving you tailored recommendations instead of generic ones.

Embeded Finance

Embedded finance simply means that financial services, like getting a loan or making a payment, are built directly into other apps or websites you already use, instead of you having to go to a separate bank or financial institution.

For example, when you’re shopping online, instead of leaving the e-commerce site to apply for a loan or use a different payment app, you might be offered instant credit or a “buy now, pay later” option right there at the checkout, making the financial transaction a seamless part of your shopping experience.

Blockchain and CBDCs

Imagine blockchain as a super secure, shared digital notebook where every transaction is recorded. This notebook is copied and stored on many computers, making it nearly impossible to tamper with, as any change would need to be approved by most copies. Now, imagine if a country’s central bank decided to issue its own digital cash, like a digital version of the rupee, directly to people and businesses, instead of just printing physical money. This is a Central Bank Digital Currency (CBDC).

By using blockchain-like technology, CBDCs could make digital payments much faster, cheaper, and more secure, allowing money to be transferred directly between people without needing many intermediaries, ultimately revolutionizing how we pay for things.

Enhanced Security

Imagine your digital bank becoming even safer in the future! This will happen because of three main things: first, new ways to confirm it’s really you, like using your unique fingerprint or face scan (biometric authentication) will get much better and harder to fool. Second, banks will use smart computer programs (AI-driven fraud detection) that can instantly spot and stop any unusual or suspicious activity in your account, often before you even notice.

Finally, the overall protection against online threats (cybersecurity) will keep improving, creating stronger digital shields around your money and personal information. All these advancements together will make digital banking incredibly secure, giving you even more peace of mind.

Greater Financial Inclusion

Digital banking is a game-changer for people who don’t have easy access to traditional banks, especially those in remote villages or rural areas. Because digital accounts can be opened and managed entirely online using a smartphone, it removes the need for physical bank branches.

This means more people can easily open a bank account, save money securely, receive direct benefit transfers from the government, and even access small loans, ultimately helping them become a part of the formal financial system and improve their economic well-being.

Conclusion:

Digital savings accounts are more than just a convenience; they are a powerful tool for modern money management. Offering instant access, attractive interest rates, lower fees, and a host of smart features, they empower individuals to take greater control of their finances and build a more secure financial future.

Pingback: IPhone Locked Here is How to Unlock IOS Devices [2025]

Pingback: A Quick start Budgeting Plan- Master your Money in 7 days