Banking Sector plays an important role in the economic development of the country. Basically, the economic development of the country depends upon the savings and investments. So, in short, higher the savings higher will be the investment. As a result, there will be high economic growth. Banking sector acts as a backbone of the financial system of a country.

What is a Banking sector?

A Banking sector is a financial institution that acts as a bridge between people who have enough money for deposit and people who needs money for various purposes. Banking services may include accepting deposits, lending money and offering various financial products like savings account, loans, credit cards etc. According to Indian Companies Act 1949,

“The accepting for the purpose of lending or investment of deposits of money from the public repayable on demand or otherwise and withdrawal by cheque draft order.”

This definition implies that the main function of a bank is acceptance of deposit from the public and advancement of loan to business and public. Further, Commercial banks are different from Industrial banks. Commercial Banks generally provide short term credit to public for various business purposes to meet their working capital requirements. On the other hand, Industrial Banks generally provide long term credit to various industries to meet their fixed capital requirements.

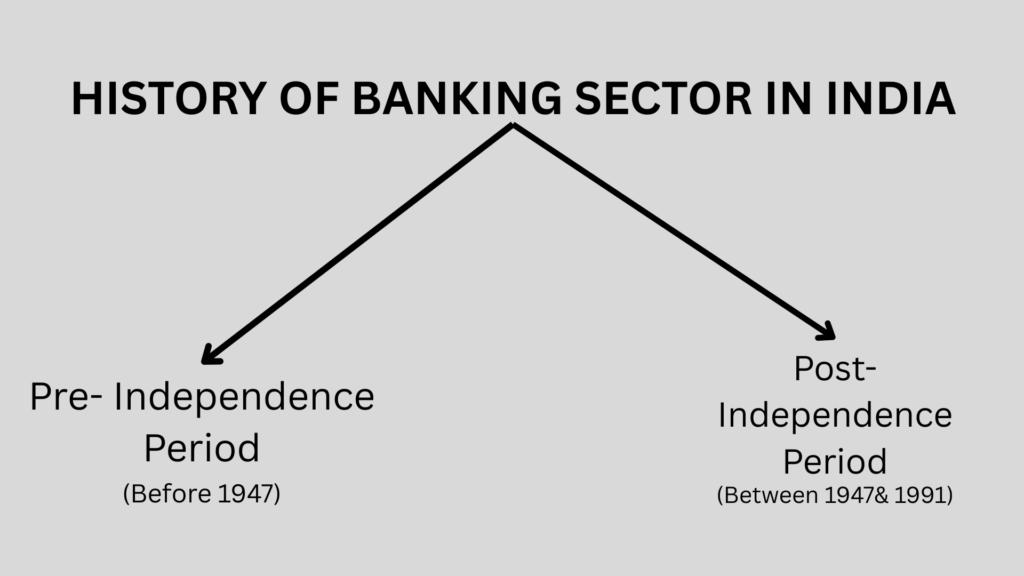

History of Banking Sector of India

Here is a pictorial representation of evolution of Indian Banking System over the years.

The journey of Banking sector of India can be divided into 2 different phases, which are described as under.

Phase 1: Pre- Independence Period (Before 1947).

Phase 2: Post- Independence Period (Between 1947 & 1991)

- Phase 1(Pre- Independence Period):The first bank, Bank of Hindustan was established in 1770, followed by The General Bank of India in 1786. The East India company established Bank of Bengal (1809), Bank of Bombay (1840), and Bank of Madras (1843) as independent units and called them presidency banks. These 3 banks were amalgamated in 1920. Between 1906 and 1913, Bank of India, Central Bank of India, Bank of Baroda, Canara Bank, and Bank of Mysore were set up. At last, The Bank of All Banks, The Reserve Bank of India has been established in 1935.

- Phase 2(Post- Independence Period):The Government of India has taken major steps to reform Indian Banking Sector after independence. The government constituted the State Bank of India to act as the principal agent of the RBI and to handle banking transactions of the Union government and state governments all over the country. In 1969, 14 commercial banks in the country were nationalized. In the second phase of banking sector reforms, seven more banks were nationalized in 1980. With this, 80 percent of the banking sector in India came under the government ownership.

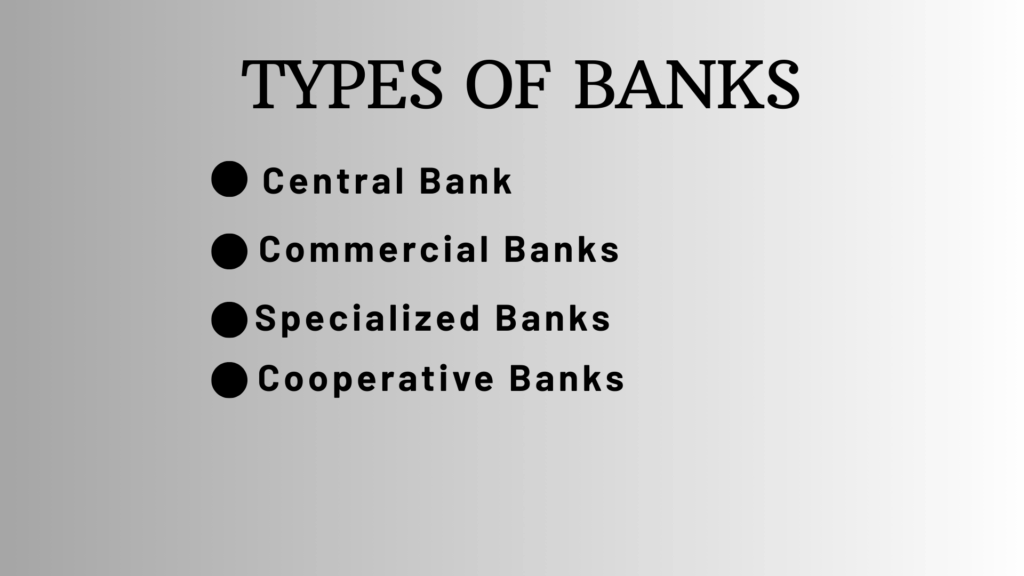

4 Different Types of Banks in India

There are various types of Banks in India. Among them, there are 4 Banks which plays a vital role in the growth and development of the country’

- CENTRAL BANK: The Central Bank is Reserve Bank of India. Most countries have their own central banks that regulates the functioning of all the other banks. RBI (Reserve Bank of India) acts as an apex bank of the country. It also plays an important role as a banker of the Government. It is owned by India’s Ministry of Finance. Its headquarters are in Mumbai. It was established in 1935.

- COMMERCIAL BANKS: Commercial Banks are organized under the Banking Companies Act, 1956. These Banks perform various functions for the public. They accept the deposits of public and also grant loans to them. The main objective of commercial banks is to generate profits. These Banks are owned by State or Government itself. The main source of income for commercial bank is public deposits. Commercial Banks can be further classified into three categories. i.e. Private Sector Banks, Public Sector Banks, Foreign Banks.

- SPECIALIZED BANKS: These banks are designed to do some specific economic activities. The primary aim of these banks is to meet the special needs of individuals, business or industries which are not fulfilled by other commercial banks. These banks focus on some important areas such as agriculture, export import trade, small businesses, or housing. These banks also help in the growth and development of the economy. FOR EXAMPLE, A Specialized bank for agriculture provides loans to farmers for seeds, equipment, irrigation facilities.

- COOPERATIVE BANKS: These banks are financial institutions that belong to its own members. The members of cooperative banks are its customers and its owners simultaneously. Cooperative Banks are established under the State Cooperative Societies Act. The Reserve Bank of India also regulates these banks. These banks play an important role in providing financial resources to the rural population.

Also Read: How inflation changed in 1990 vs 2025.

What Type of Sector is Banking?

Banking sector falls under the tertiary or service sector of the economy. This sector provides its services to primary as well as secondary sectors also. This sector includes various services like banking, transportation, communication etc.

Here are some points which shows how banking sector is considered as tertiary sector.

SERVICE- ORIENTED: Banks provides various services to individuals and businesses. These services include accepting deposits, granting loans, and other financial services.

ECONOMIC GROWTH: Banks play an important role in the economy by enabling transactions, and supporting various economic activities. this helps in the economic growth and development of the country.

What is Bank Marketing?

Bank marketing is a special field of marketing in which various services are provided to the customers in order to fulfill their financial as well as other needs. It also discusses the importance of market research, segmentation, and developing a marketing mix for banking services. Different banks offer different benefits by offering different schemes which can take care of different wants of the customers.

Purpose of Marketing Bank Services: The main purpose of marketing bank services can be explained as below:

- To identify the most profitable markets in present or in future.

- To meet the present and future needs of the customers.

- To manage and promote various products and services.

- Adapting according to changing environment.

Marketing Mix in Banking Sector of India

Banking services are all about money in different terms such as lending, depositing etc. The structure of banking services affects the success of institution in long term. The formulation of marketing mix is just like the combination of ingredients, spices in the cooking process.

7Ps of Marketing Mix in Banking Sector of India

7Ps of marketing mix includes Product, Price, Place, Promotion, People, Processes, Physical evidence. This forms the base of banking sector.

- PRODUCT: In banking, product refers to the financial services and instruments offered to customers. These are often intangible in nature. Example: Saving accounts, Current accounts, Fixed deposits, Recurring deposits, Loans (personal, home business), Credit cards, Debit cards, Online banking, Mobile banking etc. Banks needs to design and offer products that meets the needs of different customers. Product innovation, features, benefits, and bundling of services are key considerations.

- PRICE: In banking, price refers to the cost of the financial products and services which are offered by banks to its customers. Example: Interest rates on loans and deposits, account maintenance fees, transaction charges, ATM withdrawal fees, processing fees for loans and other service charges. Pricing strategies in banking are influenced by various elements such as competitor pricing, cost of funds etc.

- PLACE: Place refers to the distribution channels and locations where customers can access banking services. Example: Physical bank branches, ATM networks, online banking websites, mobile banking applications, call centers, partnership with other businesses (e.g. for bill payments). Its main aim is to provide banking services to its customers in easily and convenient way. The rise of digital banking has significantly expanded the “place” beyond physical locations, offering 24/7 access.

- PROMOTION: In banking, promotion refers to all the communication strategies which are used by different banks to inform, persuade, and remind customers about their products and services. Example: Advertising (TV, print, digital, social media), public relations, sales promotions (e.g., special interest rates for a limited period), direct marketing (emails, SMS), content marketing (financial literacy articles, blogs), personal selling (interactions with bank staff), and sponsorships.

- PEOPLE: This includes all individuals who interact with customers, as well as the customers themselves. Example: Bank employees (tellers, customer service representatives, loan officers, branch managers), who deliver the service and represent the bank’s brand.

- PROCESS: Process refers to the procedures, mechanisms, and flow of activities involved in delivering banking services. Example: Account opening procedures, loan application and approval processes, online banking workflows, Well-designed and efficient processes lead to faster service delivery, reduced errors, and improved customer satisfaction.

- PHYSICAL EVIDENCE: Physical evidence refers to the tangible aspects with which customers interact. Example: The appearance and layout of bank branches, ATM machines, bank statements, credit and debit cards (design and quality), brochures etc.

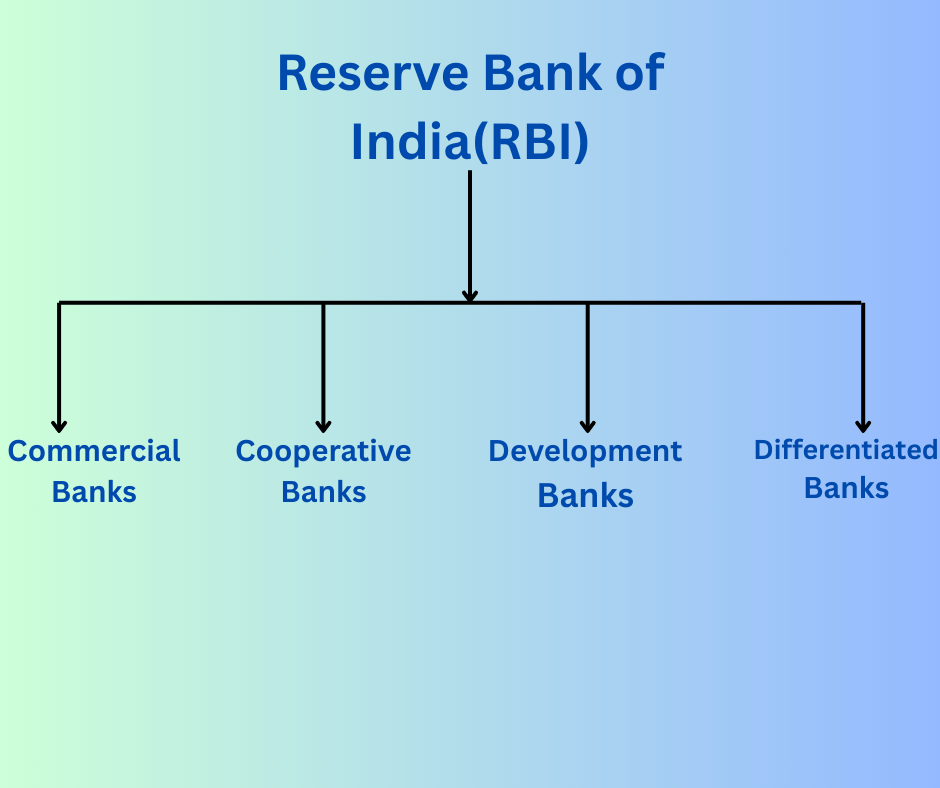

Structure of Banking Sector of India

The Reserve Bank of India (RBI) sits at the top of the structure of the Banking Sector in India and acts as the central bank of India

Reserve Bank of India (RBI): Reserve Bank of India (RBI) is the central bank of India. It is the apex bank of the Indian banking system. It is owned by Union Ministry of Finance. It acts as a regulatory body. It is responsible for regulation of Indian Banking system as well as control, issuing and maintaining money supply in the Indian economy.

- COMMERCIAL BANKS: Commercial Banks refer to those banks under the Banking Sector of India that run on a commercial basis. It means that they operate and offer services to earn a profit. They are regulated under the Banking Regulation Act, 1949.

- COOPERATIVE BANKS: Cooperative Banks refer to those financial institutions under the Banking System in India that operate on the principles of cooperation and mutual benefit for their members. They belong to their members who are both the owners and customers of the bank. Thus, it can be said that the customers are the owners of these banks. Cooperative Banks are named so because these have the cooperation of stakeholders

- DEVELOPMENT BANKS: Development Banks are also known as Term-Lending Institutions (TLIs) or Development Finance Institutions (DFIs). They are specialized financial institutions under the Banking System in India that provide long-term finance and support to the sectors of the Indian economy which possess higher risks.

- DIFFERENTIATED BANKS: Differentiated Banks under the Indian Banking System refer to those banks that cater to a specific segment of customers. The concept of Differentiated Banks was introduced in the Banking System in India by the RBI based on the recommendations of the Nachiket Mor Committee in 2013 in order to offer specialized services.

What is Digital Banking?

Digital banking in India refers to using online and mobile technologies to conduct various banking activities and transactions. It encompasses various services like accessing accounts, making payments, transferring funds, checking balances, and applying for loans, all through digital channels like websites and mobile apps. It enables customers to access almost all financial services 24/7, without visiting a physical bank branch.

Types of Digital Banking

Digitalization in banking sector of India effects the whole economy. There are various types of digital baking which are described as under.

- Online Banking (Internet Banking or Net Banking): This is one of the earliest forms of digital banking. It allows customers to perform banking transactions and access services through a bank’s secure website using a web browser on a computer or laptop. Key features include checking account balances, viewing transaction history, transferring funds between accounts (both within the same bank and to other banks via methods like NEFT, RTGS, IMPS), paying bills, and managing account details.

- Mobile Banking: This is also an important type of digital banking. Here all the banking transactions can be easily done by using bank’s official app on your own smartphone or tablet. These apps are specially designed to be use on a mobile screen. It offers various services such as checking balances, transfer funds, paying bills etc.

- UPI (Unified Payment Interface): It allows users to transfer their money between different accounts using mobile phone or tablet. You can link multiple bank accounts to one UPI app (like Google Pay, Phone Pe, Paytm, or the BHIM app). The user can send or receive money using a simple identifier called a Virtual Payment Address (VPA) or by scanning a QR code. It’s widely used for small and large payments to friends, family, or businesses.

- Mobile Wallets: These are like digital purses on your phone where you can store money to make quick payments. You can add money to these wallets from your bank account or cards. They are often used for paying for things online, at shops by scanning QR codes, recharging your phone, paying utility bills, and more. Examples include Paytm Wallet, Mobikwik, etc.

- Banking Cards (Debit Cards, Credit Cards, Prepaid Cards): These cards are key tools for digital transactions. DEBIT CARDS are linked directly to your bank account. It further allows a user to pay at shops using card machine or online and also withdraw cash from ATMs. CREDIT CARDS allow users to buy anything in present and make payment sometimes in future. It is useful for both online and offline purchases. PREPAID CARDS are used by users to load money onto these cards beforehand and can only spend the amount loaded. These cards are not directly linked to your bank accounts.

- Other Digital Payment methods: The following are the other digital methods which are used for making payments online.

- IMPS, NEFT, RTGS: These are systems used for transferring funds between bank accounts. IMPS is for instant transfers (24/7), while NEFT and RTGS are for transferring funds in batches or for large amounts, respectively (also mostly 24/7 now). These are often accessed through Internet or Mobile banking.

- Aadhaar Enabled Payment System (AEPS): This allows basic banking transactions like cash withdrawal, balance inquiry, and fund transfer using your Aadhaar number and biometric authentication (like fingerprint) at a banking correspondent or micro-ATM. This is particularly helpful in rural areas.

- Point of Sale (PoS) Terminals: These are the card swipe machines you see at shops, enabling you to pay using your debit or credit card digitally.

Conclusion: In the end, we can conclude that banking sector of India becomes more and more digital. With the help of new technology, doing banking transactions becomes easy while using mobile phone or computer. While there will still be challenges, like keeping things safe online, banking is changing a lot to include more people and make managing your money smooth and simple.

Pingback: 10 Best Career options after B.com for successful life

Pingback: 24/7 availability of digital savings account